1.0 INTERNAL AUDIT UNIT (IAU)

IAU is one of the Unit of MOFA established by the Chief Director in line with Public Financial Management Act 2016, Act 921.

1.1 MISSION OF IAU

Internal Audit’s mission is to contribute to the efficient, economical and effective operation and realized the objectives of the Ministry: its directorates, agencies, programmes and projects; as well as to encourage and promote the highest level of professionalism and integrity, while providing reliable professional advice, independent and objective assurance services of the highest standard of the system of internal control.

1.2 VISION OF IAU

The IAU is committed to provide independent, objective assurance, value-added audit and consultancy services to assist management and improve operations in the achievement of the Ministry’s objectives.

1.3 OBJECTIVES OF IAU

The objectives of the IAU are to assist all levels of Management in the effective discharge of their responsibility performing audits in an objective and analytical manner, in accordance with International Auditing Standards, IAA Directives / Regulation / Frameworks and furnishing management with reports on analyses, appraisals, and recommendations on the audited activities.

1.4 CRITICAL SUCCESS FACTORS

The critical success factors are the key activities or processes that are required to enable the IAU achieve its strategic goals in line with the relevant public financial management enactments. The following are critical factors emerged from the prognosis of the IAU:

- Availability of budgetary allocation;

- Effectiveness of the Audit Committee;

- Principal Spending Officer (PSO) towards the IAU;

- Management’s cooperation with the IAU:

- provision of information for audit work

- responsiveness to audit observations

- willingness to implement recommendations

- Qualification, CPD and number of internal auditors available; Independence of the IAU.

1.5 OVERVIEW OF MANAGEMENT EXPECTATIONS

The primary expectation of management of the Internal Audit Unit as specified in section 83(3) of the Public Financial Management Act, 2016 (Act 921). In addition, management expects the IAU to at all times act within the professional code of ethics as stipulated under the International Standards for the Professional Practice of Internal Auditing.

1.6 AUDIT REPORTING

1.6.1 Assignment level

A report on each assignment (Planned or Special Audit) would be prepared by the Team Leader, reviewed by a supervisor before submission to the Directors or Project Coordinators.

1.6.2 Organisational Level

A final report would be submitted to the Chief Director upon completion of an audit exercise. The Head of Internal Audit would get the PSO to sign transmittal letters to the mandated recipients.

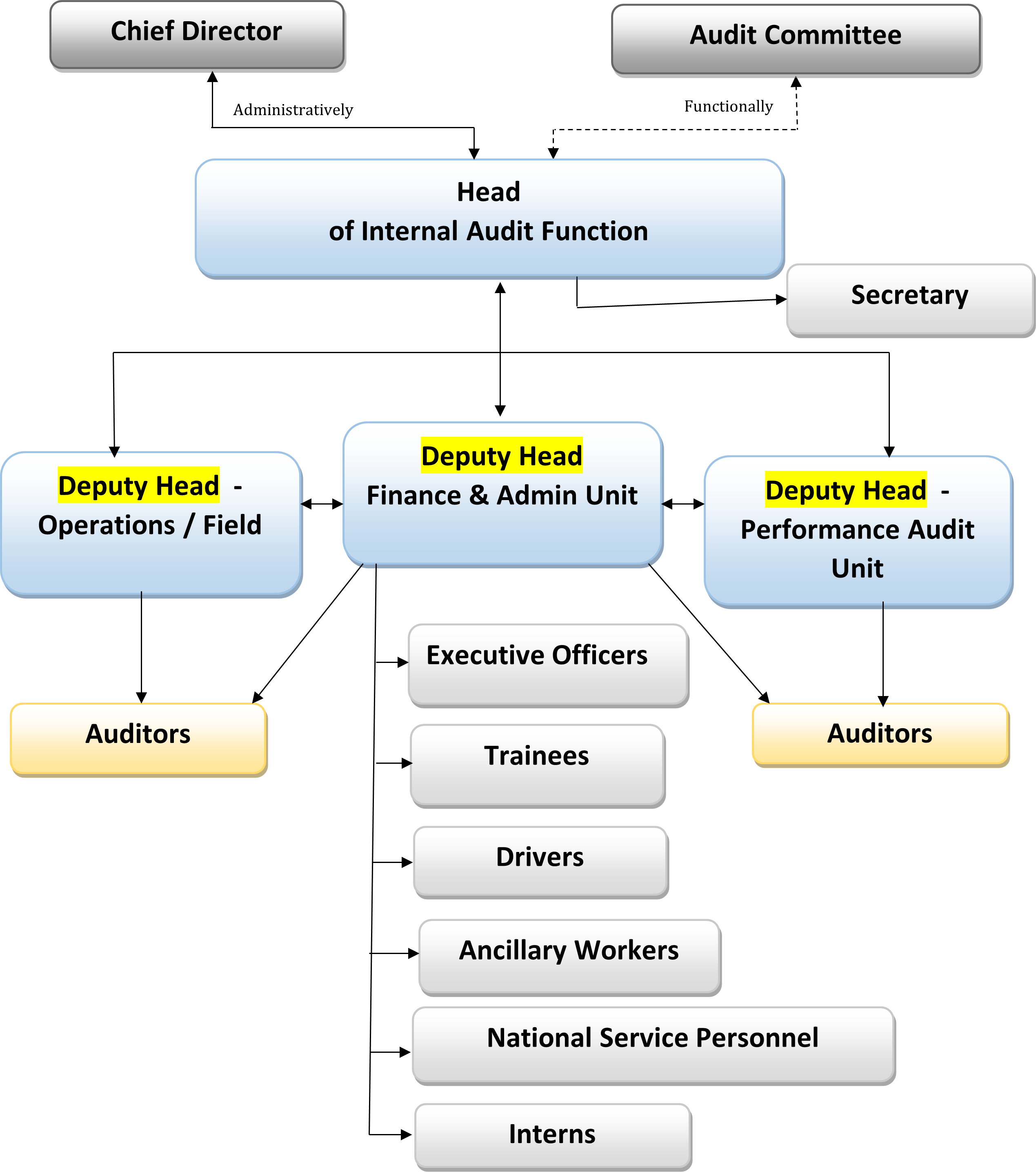

1.7 STRUCTURE OF THE INTERNAL AUDIT UNIT

The Chief Internal Auditor currently is the Head of the Unit and is assisted by the most senior Internal Auditor, then other and Assistant Audit Trainee.

|

No. |

Name |

Grade |

Qualification |

|

1. |

Isaac Adjin Bonney |

Chief Internal Auditor |

BBA, MFC, ICAG, CPFA |

|

2. |

Edwin Emmanuel Bentum |

Snr. Internal Auditor |

MBA Acct. |

|

3. |

Winifred Aduamoah |

Snr. Internal Auditor |

BSc Acct. |

|

4. |

Jonas Hammond |

Snr. Internal Auditor |

BSc Acct. |

|

5. |

Abigail Osae |

Internal Auditor |

BBA Accounting |

|

6. |

Nii Kpakpa Sakyi-Quartey |

Internal Auditor |

BSc Math. |

|

7. |

Delphine Nana Adjoa Obeng |

Asst. Internal Auditor |

HND Acct. |

|

8. |

Naomi Donnie Amenyah |

Asst. Internal Auditor |

BSc. Bus. Admin |

|

9. |

James Adjettey Sowah |

Asst. Internal Auditor |

BSc. Acct. |

|

10. |

Eric Oduro Asante |

Asst. Internal Auditor |

BSc. Acct. |

|

11. |

Solomon Amenyo |

Asst. Internal Auditor |

BSc. Acct. |

|

12. |

Joana Esinam Bedzo |

Asst. Internal Auditor |

BCom |

|

13. |

Sylvester Yeboah |

Asst. Internal Auditor |

BBA Acct. |

|

14. |

Bright Seyram Adzoma |

Asst. Internal Auditor |

MBA Finance |

|

15. |

Ebenezer Hagan |

Principal Executive Officer |

HND |

|

16 |

Beatrice Osei Paibi |

Private Secretary |

Appendix Below depicts the structure of the Internal Audit Unit.